WHAT IS LIFE CYCLE COSTING?

- Life cycle costing is the process of compiling all costs that the owner or producer of an asset will incur over its lifespan.

- These costs include the initial investment, future additional investments, and annually recurring costs, minus any salvage value.

- Whole-life costing covers an asset’s costs from the time you purchase it to the time you get rid of it.

- The cost to buy, use, and maintain a business asset adds up. Whether you’re purchasing a car, a copier, a computer, or inventory, you should consider and budget for the asset’s future costs.

PURPOSE OF LIFE CYCLE PROCESS

As mentioned, conducting a life cycle cost analysis helps you estimate how much an asset will cost you over the course of its life.

Take a look at some of the reasons why knowing an asset’s total cost can guide your business decisions.

Take a look at some of the reasons why knowing an asset’s total cost can guide your business decisions.

1. Choose between two or more assets

Using life cycle costing helps you make purchasing decisions. If you only factor in the initial cost of an asset, you could end up spending more in the long run. For example, buying a used asset might have a lower price tag, but it could cost you more in repairs and utility bills than a newer model.

Life cycle cost management depends on your ability to make a smart investment. When you are deciding between two or more assets, consider their overall costs, not just the price tag in front of you.

2. Determine the asset’s benefits

How do you know if you should buy an asset? Generally, you weigh the pros and cons of your purchase. But if you only consider the initial, short-term cost, you won’t know if the asset will benefit your business financially in the long run.

By using life cycle costing, you can more accurately predict if the asset’s return on investment (ROI) is worth the expense. If you only look at the asset’s current purchase cost and don’t factor in future costs, you will overestimate the ROI.

3. Create accurate budgets

When you know how much an asset’s total price is, you can create budgets that represent your business’s actual expenses. That way, you won’t underestimate your business’s costs.

A

budget is made up of expenses, revenue, and profits. If you underestimate an

asset’s cost on your budget, you are overestimating your profits. Failing to

account for expenses can result in overspending and negative cash flow.

Looking

for a simple way to track your business’s costs? Patriot’s online accounting

software is made for the non-accountant, making it easy to track your expenses.

And, we offer free, U.S.-based support. Try it for free today!

LIFE CYCLE COSTING PROCESS

Conducting a life cycle cost assessment helps you better predict how much your business will pay when you acquire a new asset.

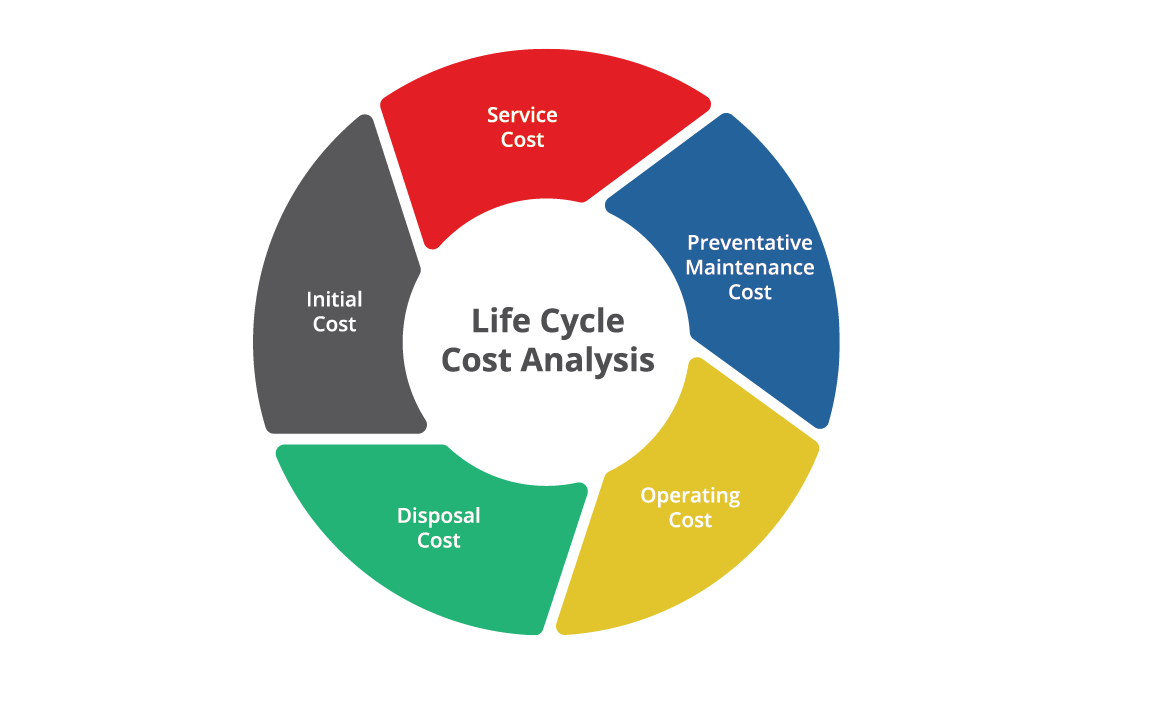

To calculate an asset’s life cycle cost, estimate the following expenses:

- Purchase

- Installation

- Operating

- Maintenance

- Financing (e.g., interest)

- Depreciation

- Disposal

BENEFIT OF LIFE CYCLE PROCESS

Following are the main benefits of product life cycle costing:

(i) It results in earlier action to generate revenue or lower costs than otherwise might be considered. There are a number of factors that need to be managed in order to maximise return in a product.

(ii) Better decision should follow from a more accurate and realistic assessment of revenues and costs within a particular life cycle stage.

(iii) It can promote long term rewarding in contrast to short term rewarding.

(iv) It provides an overall framework for considering total incremental costs over the entire span of a product.

EXAMPLE OF LIFE CYCLE COSTING ASSESSMENT

- Life-Cycle Cost Analysis (LCCA) Method

The purpose of an LCCA is to estimate the overall costs of project alternatives and to select the design that ensures the facility will provide the lowest overall cost of ownership consistent with its quality and function. The LCCA should be performed early in the design process while there is still a chance to refine the design to ensure a reduction in life-cycle costs (LCC).

The first and most challenging task of an LCCA, or any economic evaluation method, is to determine the economic effects of alternative designs of buildings and building systems and to quantify these effects and express them in dollar amounts.

- Costs

There are numerous costs associated with acquiring, operating, maintaining, and disposing of a building or building system. Building-related costs usually fall into the following categories:

- Initial Costs—Purchase, Acquisition, Construction Costs

- Fuel Costs

- Operation, Maintenance, and Repair Costs

- Replacement Costs

- Residual Values—Resale or Salvage Values or Disposal Costs

- Finance Charges—Loan Interest Payments

- Non-Monetary Benefits or Costs

1. INITIAL COSTS

Initial costs may include capital investment costs for land acquisition, construction, or renovation and for the equipment needed to operate a facility.

2. ENERGY AND WATER COSTS

Operational expenses for energy, water, and other utilities are based on consumption, current rates, and price projections. Because energy, and to some extent water consumption, and building configuration and building envelope are interdependent, energy and water costs are usually assessed for the building as a whole rather than for individual building systems or components.

3. OPERATION, MAINTENANCE, AND REPAIR COSTS

Non-fuel operating costs, and maintenance and repair (OM&R) costs are often more difficult to estimate than other building expenditures. Operating schedules and standards of maintenance vary from building to building; there is great variation in these costs even for buildings of the same type and age. It is therefore especially important to use engineering judgment when estimating these costs.

4. REPLACEMENT COSTS

The number and timing of capital replacements of building systems depend on the estimated life of the system and the length of the study period. Use the same sources that provide cost estimates for initial investments to obtain estimates of replacement costs and expected useful lives. A good starting point for estimating future replacement costs is to use their cost as of the base date. The LCCA method will escalate base-year amounts to their future time of occurrence.

5. RESIDUAL VALUES

The residual value of a system (or component) is its remaining value at the end of the study period, or at the time it is replaced during the study period. Residual values can be based on value in place, resale value, salvage value, or scrap value, net of any selling, conversion, or disposal costs. As a rule of thumb, the residual value of a system with remaining useful life in place can be calculated by linearly prorating its initial costs. For example, for a system with an expected useful life of 15 years, which was installed 5 years before the end of the study period, the residual value would be approximately 2/3 (=(15-10)/15) of its initial cost.

6. OTHER COSTS

Finance charges and taxes: For federal projects, finance charges are usually not relevant. Finance charges and other payments apply, however, if a project is financed through an Energy Savings Performance Contract (ESPC). The finance charges are usually included in the contract payments negotiated with the Energy Service Company (ESCO) or the utility.

REFRENCES

- (Mohan, n.d.)Bragg, S. (2020). Life Cycle Costing. Cost Accounting. https://www.accountingtools.com/articles/life-cycle-costing.html

- How to Use Life Cycle Costing. (2020). https://www.patriotsoftware.com/blog/accounting/life-cycle-costing-process/

- Mohan, A. (n.d.). Life Cycle Costing : Meaning, Characteristics and everything else. https://www.accountingnotes.net/cost-accounting/life-cycle-costing/life-cycle-costing-meaning-characteristics-and-everything-else/5783

- Rohit Agarwal. (n.d.). Life-Cycle Costing : Meaning, Benefits and Effects. https://www.yourarticlelibrary.com/accounting/costing/life-cycle-costing-meaning-benefits-and-effects/53110